As the advertising industry braces for another Upfront cycle, the rules of engagement have changed. In The Myers Report 2025–2026 Marketing, Advertising & Media Economic Forecast, we present a stark, data-backed reality: legacy sales strategies are no longer enough. In an era defined by economic instability, media fragmentation, and performance obsession, Upfront spending is under intensifying scrutiny.

The 75-page report offers a comprehensive review of marketplace trends, economic pressures, media forecasts, and investment shifts across all major channels. Below, we spotlight the four primary forces that will shape 2025/2026 Upfront commitments — and the strategic imperatives for navigating them.

1. Economic Uncertainty and Tariff-Driven Headwinds

The reintroduction of tariffs by the Trump administration — targeting imports from China and Mexico — has rattled economic confidence across the retail, automotive, and e-commerce sectors. Advertisers are already reacting. According to industry surveys and analysis cited in The Myers Report, a significant portion of marketers anticipate reducing media budgets by 6% to 10% in the second half of 2025.

For network and streaming sellers, this means tougher conversations in the Upfront. Discretionary categories are pausing, waiting, or reallocating toward short-term ROI-driven campaigns. While some premium events (notably sports) will maintain commitments, general entertainment categories are facing contraction.

“The question isn’t ‘what’s your CPM?’ anymore,” notes Jack Myers in the report’s commentary. “It’s ‘how fast can I cancel, reallocate, or prove performance?’ Flexibility is the new currency.”

2. Performance-Driven Marketing Steals Share

Retail media. Search. Influencer. First-party data.

The growth of performance-led, commerce-enabled media is accelerating a secular trend: brands want results they can measure and models they can simulate. According to The Myers Report, retail media is expected to exceed $63.2 billion in 2025, up nearly 20% from the prior year, absorbing dollars that would have traditionally flowed through Upfront commitments.

This shift isn’t temporary. It’s systemic. More marketers are building in-house modeling tools, connecting ad delivery directly to sales lift, and pushing agencies to validate every dollar against commerce results. This creates a chilling effect for traditional Upfront negotiations, where long-term commitments often lack performance transparency.

As a result, The Myers Report forecasts a moderate decline of 8.6% in total Upfront and NewFront commitments for 2025-2026 compared to the previous cycle, particularly in general entertainment and scripted formats.

3. Media Fragmentation Complicates Reach and Efficiency

With audiences splintered across hundreds of streaming apps, social platforms, and digital communities, media buyers face a dilemma: how to maintain efficient reach when traditional mass channels are eroding?

Fragmentation has pushed advertisers to diversify their investments, often reducing Upfront commitments in favor of programmatic buys, influencer partnerships, and experiential activations that offer agility and audience specificity.

The growth of ad-supported streaming (FAST, AVOD), digital out-of-home, and commerce video further dilutes the share of Upfront dollars as attention becomes harder to pin down.

According to The Myers Report, advertisers are looking to converged video solutions that combine linear, CTV, and digital into unified buys — but are waiting for measurement consistency before committing fully in the Upfront window.

4. Technology and Targeting: Planning in the Age of Predictive AI

The rise of AI-powered planning, bid optimization, and data integration is transforming the role of the buyer — and redefining how media is valued.

Agency holding companies like Publicis, Omnicom, IPG, and Dentsu are now operating as predictive intelligence firms, with clean rooms, audience simulators, and outcome modeling capabilities that allow them to challenge pricing, cancel late, and reallocate mid-flight.

This is particularly relevant in the 2025/26 Upfront cycle, where ‘options’ clauses — allowing buyers to cancel a portion of their commitments within designated timeframes — are being pushed harder than ever.

Buyers want performance and agility. Sellers must respond with smarter packaging, outcome guarantees, and partnerships that reflect this new intelligence economy.

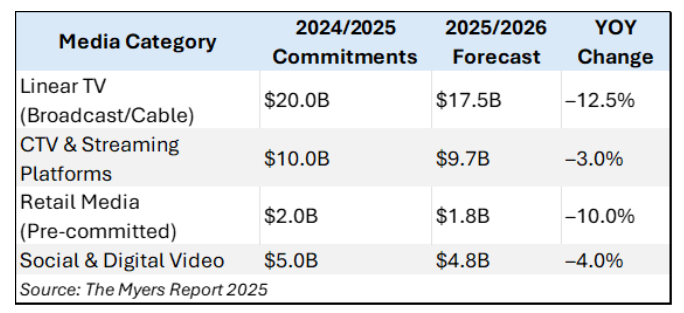

Outlook for 2025/2026 Upfront Commitments

The Myers Report outlines the following projections for year-over-year shifts in Upfront and NewFront commitments by category:

For Media Leaders: A Call to Action

Now is not the time to defend outdated models. Now is the time to reinvent how we define value.

As outlined in the Go-to-Market section of The Myers Report, network sales organizations must:

- Shift from transaction to transformation

- Lead the currency and identity conversations

- Integrate creative and commerce

- Validate impact with independent insights

This is a moment for strategic reinvention — where performance meets trust, agility meets transparency, and sellers become partners in outcomes.

Download the Full Report

📘 Corporate subscribers: your full 75-page PDF is available now. Didn’t receive it? Contact MyersReport@gmail.com.

📈 Not yet subscribed? Purchase the full report for $2,950, or subscribe to the 24-report 2025 white paper series for $6,000 (one week only at 50% off. Contact jm@jackmyers.com for discount):

👉 www.myersreports.com

📬 For speaking engagements, strategy briefings, or leadership workshops, contact Jack Myers at jm@jackmyers.com.